How to Stop Foreclosure Fast in Portland

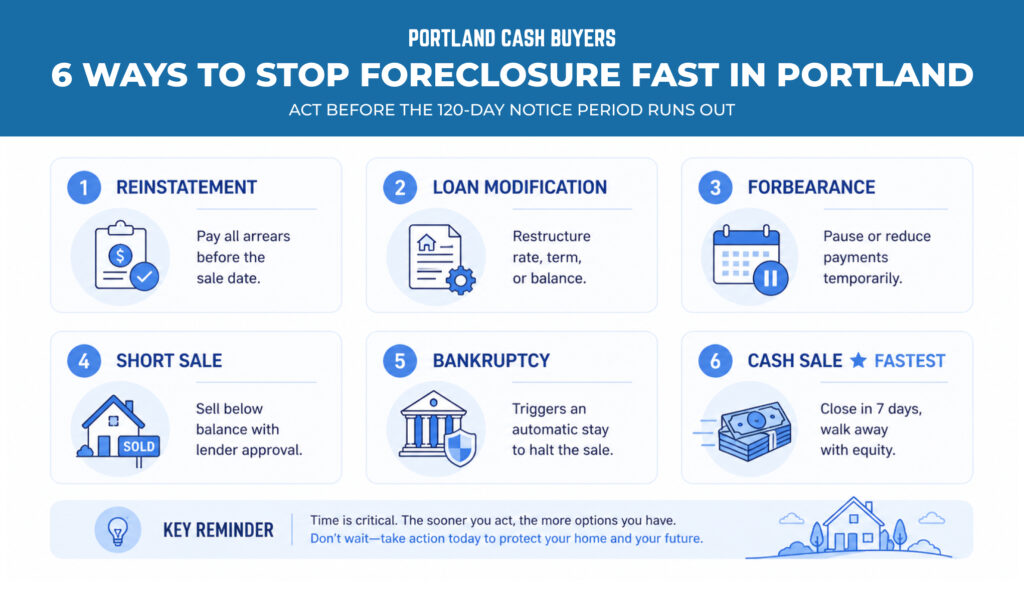

To stop foreclosure fast in Portland, you have six real options: reinstatement, loan modification, forbearance, short sale, bankruptcy, or a cash sale. Here is a quick summary before we break each one down:

- Reinstatement: Pay all past-due amounts before the sale date

- Loan modification: Restructure the loan terms with your lender

- Forbearance: Temporarily pause or reduce payments

- Short sale: Sell for less than you owe with lender approval

- Bankruptcy: Automatically delay the process while you reorganize

- Cash sale: Sell your home quickly and walk away with equity intact

Time is the most critical factor here. Oregon operates under a nonjudicial foreclosure process, which means the bank does not need a court order to proceed. Once a Notice of Default is recorded, you may have as few as 120 days before the auction date. Acting now is not optional.

If you are already facing this situation, the facing foreclosure page at Portland Cash Buyers explains how a cash sale can stop the process before it reaches the courthouse steps.

Option 1: Reinstatement. Pay What You Owe

Reinstatement means catching up on every missed payment, plus fees and late charges, in one lump sum. Under Oregon law, you can reinstate your loan at any point up to five days before the scheduled trustee sale.

This option works well if you had a temporary setback — a job interruption, a medical bill, or a gap in income — and your finances have since recovered. However, if you cannot fund the full arrearage, reinstatement is off the table.

Pro Tip: Contact your servicer in writing before attempting reinstatement. Request a formal reinstatement quote, which will show the exact payoff amount including fees. Verbal estimates are often inaccurate and not binding.

Option 2: Loan Modification

A loan modification permanently changes one or more terms of your mortgage — interest rate, loan term, or principal balance. Lenders are not required to grant one, but federal servicing rules do require them to evaluate your application before proceeding with foreclosure.

The application process can take weeks. Additionally, you typically cannot have an active foreclosure sale scheduled while a complete modification application is under review. Submit documentation quickly and follow up consistently to keep the review open.

Option 3: Forbearance

Forbearance is a temporary agreement where your servicer lets you pause or reduce payments for a set period — usually three to twelve months. Consequently, you will owe the deferred amount at the end of the forbearance window, either as a lump sum or tacked onto future payments.

This option buys time, but it does not erase what you owe. If your hardship is ongoing rather than temporary, forbearance may simply delay the problem rather than resolve it.

Option 4: Short Sale

In a short sale, you sell the property for less than the outstanding mortgage balance, and the lender agrees to accept the proceeds as full or partial satisfaction of the debt. This requires lender approval and can take two to four months to complete.

A short sale does less damage to your credit than a completed foreclosure. However, the timeline is not always compatible with stopping a fast-moving foreclosure. Oregon law also requires specific disclosures to buyers in judicially foreclosed short sales. Furthermore, any tax consequences depend on your specific situation — consult a tax professional.

Option 5: File for Bankruptcy (Temporary Stop)

Filing for Chapter 13 bankruptcy triggers an automatic stay, which legally halts all collection actions, including foreclosure. This can immediately freeze the process and give you time to reorganize your finances under a court-supervised repayment plan.

Chapter 13 does not eliminate the debt. Instead, it restructures it over three to five years. Notably, a bankruptcy on your record can affect your credit for up to ten years, making it harder to buy another home or obtain financing in the future. Use this option as a strategic pause, not a permanent solution.

Option 6: Sell to a Cash Buyer Fast

Selling your home for cash is often the fastest and cleanest path out of foreclosure. A direct cash buyer can close in as little as 7 days — well within Oregon’s 120-day notice period. You receive the equity you have built, avoid a foreclosure on your record, and walk away without repairs, showings, or agent commissions.

This option works even if you are significantly behind on payments. A cash buyer works directly with your lender to stop the foreclosure process before the auction date. As a result, your credit stays intact and you retain control over the outcome.

Pro Tip: Request a cash offer before you exhaust your other options. Getting an offer costs nothing and gives you a concrete fallback. You can still pursue a modification or reinstatement in parallel, and if those fall through, you have a closing date already in place.

The Oregon Foreclosure Timeline You Need to Understand

Understanding the timeline is critical to stopping foreclosure fast in Portland. Here is how Oregon’s nonjudicial process typically unfolds:

| Stage | Approximate Timing |

|---|---|

| First missed payment | Day 1 |

| Servicer contacts you about loss mitigation | Within 36 days of missed payment |

| Resolution conference notice sent | Before Notice of Default |

| Notice of Default recorded | After lender exhausts resolution conference |

| Notice of Sale served | At least 120 days before sale |

| Reinstatement deadline | 5 days before sale |

| Trustee sale / auction | Day 120+ after Notice of Sale |

Most nonjudicial foreclosures in Oregon take approximately 150 days from start to sale. That figure does not include the months of nonpayment that typically precede a Notice of Default. In practice, many Portland homeowners have more time than they realize — but only if they take action immediately.

Why a Cash Sale Is Often the Best Choice for Portland Homeowners

Each option above has merit in the right situation. However, for homeowners who are deep in arrears, cannot qualify for a modification, or simply need to move quickly, a cash sale consistently outperforms the alternatives.

Here is why:

- Speed. A cash buyer can close in as little as 7 days. No financing contingencies, no waiting for underwriting.

- Certainty. Traditional sales fall through regularly due to financing issues. A cash offer is guaranteed.

- No repairs. You sell as-is. No cleaning, staging, or contractor work required.

- No fees. No agent commissions (which typically run 5–6% of the sale price), no closing costs.

- Equity preserved. If your home has equity, a cash sale puts that money in your hands — not the bank’s.

For Portland homeowners who are late on mortgage payments, a cash sale stops the clock. Once the sale closes, the foreclosure process ends.

How Portland Cash Buyers Helps You Stop Foreclosure

Portland Cash Buyers has worked with homeowners in foreclosure since 2004. Owner Quinn Irvine handles every transaction personally and has helped over 1,000 Portland families avoid foreclosure, protect their credit, and move forward.

The process is direct:

- You share your property address and situation — takes 30 seconds.

- Quinn assesses the property and delivers a no-obligation cash offer within 24 hours.

- You pick your closing date. Closings are handled through a licensed title company.

There are no agent fees, no commissions, no repair requirements, and no surprise deductions at closing. Portland Cash Buyers is BBB A+ accredited and Google 5-star rated. Quinn works with your lender directly to stop the foreclosure process and get the sale closed on your schedule.

If you are weighing whether to sell before the auction, the sell house before foreclosure auction guide walks through how the timing works in detail.

Frequently Asked Questions About How to Stop Foreclosure Fast in Portland

How many days before foreclosure can I sell my house in Portland?

In Oregon, you can sell your home any time before the trustee sale, right up to closing day. A cash buyer can close in 7 days, giving you flexibility even close to the auction date.

Will selling my house stop foreclosure from appearing on my credit?

Yes. If you close a sale before the foreclosure is completed, it typically does not appear as a foreclosure on your credit report. A short sale or cash sale closes the loan without a completed foreclosure.

Can I stop foreclosure if I owe more than my house is worth?

Possibly. A short sale requires lender approval when you are underwater. A cash buyer may still be able to help by working directly with your lender to negotiate a resolution before the sale.

Does filing for bankruptcy stop foreclosure in Oregon?

Filing Chapter 13 bankruptcy triggers an automatic stay that legally halts foreclosure proceedings. However, it does not eliminate the debt — it restructures repayment over three to five years under court supervision.

How fast can Portland Cash Buyers close on my home?

Portland Cash Buyers can close in as few as 7 days. The timeline is based on your situation and the title process, not financing delays or buyer mortgage approvals.

How to Stop Foreclosure Fast in Portland: Your Next Step

Knowing how to stop foreclosure fast in Portland means nothing without action. The earlier you move, the more options remain open to you. Whether you pursue reinstatement, a modification, or a cash sale, the window is smaller every day you wait.

Portland Cash Buyers has worked with homeowners at every stage of this process — from the first missed payment to the week before the auction. There is no pressure, no obligation, and no cost to get an offer. Call Quinn directly at (503) 770-0145 or submit your address online for a response within 24 hours.

Learn more about your situation on the stop foreclosure Portland service page or explore the Oregon foreclosure timeline to understand exactly where you stand.