What Every Homeowner Must Know First about the Oregon Foreclosure Timeline

The Oregon foreclosure timeline moves faster than most homeowners expect. By the time a formal notice arrives, your options are already narrowing.

Here is a quick-reference breakdown:

- Days 1 to 90: Missed payments, late fees, and servicer outreach begin

- Day 36 to 45: Federal law requires written notice of loss mitigation options

- Day 120+: Lender can legally start formal foreclosure proceedings

- Notice of Default: Filed in county records, triggering the formal clock

- Notice of Trustee’s Sale: Served at least 120 days before auction

- Trustee’s Sale: Home is auctioned with no post-sale redemption right

For most Oregon homeowners, the total window from the first missed payment to the auction runs roughly 6 to 12 months. That feels long. It closes fast.

Nonjudicial vs. Judicial Foreclosure in Oregon

Oregon allows two types of foreclosure: nonjudicial and judicial. Understanding which applies to you shapes the entire foreclosure timeline Oregon homeowners must navigate, including how fast things move and what rights you retain.

Nonjudicial foreclosure is by far the most common method for primary residences. It follows a statutory process under Oregon Revised Statutes (ORS 86.726 through 86.815) and does not involve the courts. It is faster and cheaper for the lender, and offers no post-sale redemption right.

Judicial foreclosure goes through the courts. If the lender wins, the property is sold at auction. Homeowners get a 180-day redemption period after the sale (ORS 88.106), but this method is rarely used for residential trust deeds in Oregon.

Pro Tip: Any document labeled “Notice of Default and Election to Sell” means a nonjudicial foreclosure is underway. Contact a certified Oregon housing counselor right away before responding to anything.

Stage 1: Missed Payments (Days 1 to 90)

The Oregon foreclosure timeline does not begin with a legal notice. It begins the day you miss your first payment, and the pre-foreclosure stage is where you have the most room to act.

Most mortgage contracts include a 10 to 15-day grace period before a late fee kicks in. After that, your servicer will start calling. Federal law requires servicer phone contact no later than 36 days after a missed payment and written notice of loss mitigation options by day 45 (12 C.F.R. § 1024.39).

Loss mitigation options can include loan modifications, repayment plans, and forbearance agreements. These programs exist specifically to help homeowners avoid going deeper into the process.

Key steps to take immediately:

- Read all lender mail and respond to the servicer contact

- Contact an Oregon housing counselor through the Foreclosure Avoidance Program (OFA)

- Document every communication date and outcome

Pro Tip: If you know you cannot catch up on payments realistically, contact a cash buyer at this stage. You have the most leverage and equity now. Every additional month of arrearages and penalties shrinks what you can walk away with at closing.

Stage 2: Notice of Default

Federal law requires servicers to wait until your loan is more than 120 days delinquent before formally starting foreclosure (12 C.F.R. § 1024.41). In practice, many Oregon lenders wait five months or longer before recording the Notice of Default.

Before the NOD can be recorded, the lender must first offer you the Oregon Foreclosure Avoidance (OFA) resolution conference. This is a mediation session with the lender and a neutral mediator. It must occur within 75 days of the lender’s OFA notice (ORS 86.729). You must meet with a housing counselor beforehand and pay a fee, though waivers are available.

If no agreement is reached, the trustee records the Notice of Default in the county records. This document lists the foreclosing entity, the arrearages owed, and the scheduled sale date.

Additionally, you can still stop the process after the NOD by reinstating the loan. Oregon law allows reinstatement up to five days before the trustee’s sale (ORS 86.778).

Stage 3: Notice of Trustee’s Sale

Alongside or shortly after the NOD, the trustee serves a Notice of Trustee’s Sale. This must be delivered at least 120 days before the scheduled auction date (ORS 86.774).

The trustee also sends a “danger notice” warning you of impending home loss and publishes the sale notice in a local newspaper. At this point, the auction date is formally set.

Understanding the foreclosure timeline Oregon courts enforce matters here: once the Notice of Trustee’s Sale is served, you have exactly 120 days minus the five-day reinstatement cutoff. This stage is where many Portland-area homeowners begin weighing a sale seriously. Two viable options remain: reinstate the full loan balance or sell the property before the auction date arrives.

Stage 4: The Trustee’s Sale

The trustee’s sale is a public auction. Any bidder except the trustee can participate. The sale must take place between 9:00 a.m. and 4:00 p.m. The home goes to the highest cash bidder. If no one outbids the lender’s opening amount, the lender takes the property.

Reaching the end of the Oregon foreclosure timeline at this stage carries serious consequences:

- You lose all equity remaining above what is owed on the loan

- Oregon law provides no post-sale redemption right in a nonjudicial foreclosure (ORS 86.797)

- You must vacate within 10 days of the sale

- The foreclosure stays on your credit report for up to seven years

One protection worth noting: in a nonjudicial foreclosure, the lender cannot pursue a deficiency judgment against you even if the sale price falls short of the total loan balance. Notably, this protection disappears if you choose a short sale instead.

Pro Tip: The trustee can technically rescind the sale within 10 calendar days if the borrower and lender agree to a foreclosure avoidance measure. Do not count on this as a strategy. Negotiate well before the auction, not after.

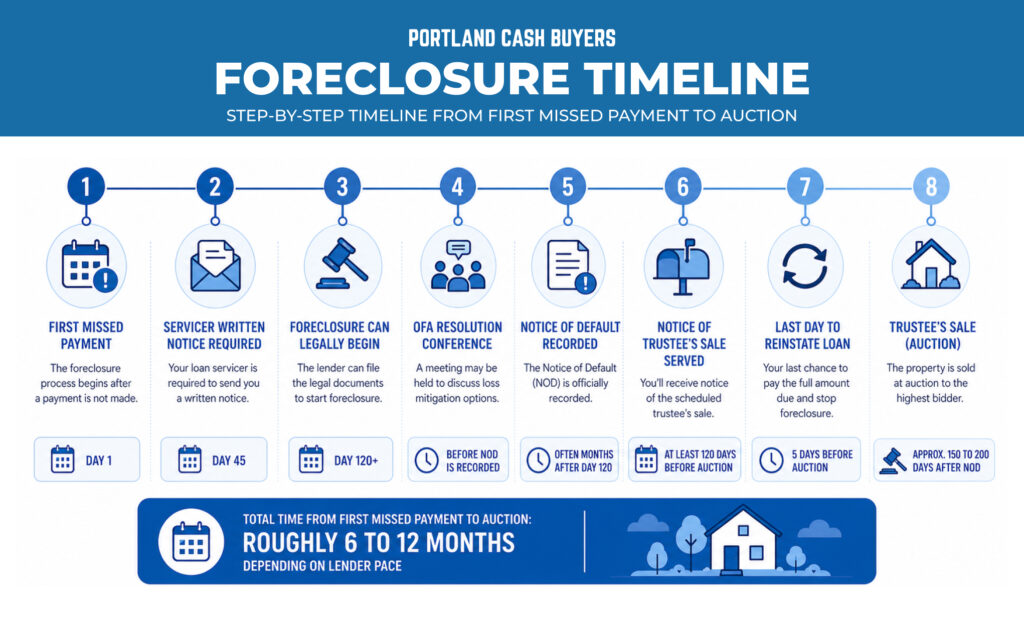

Oregon Foreclosure Timeline: Full Stage Reference

| Stage | Approximate Timing |

|---|---|

| First missed payment | Day 1 |

| Servicer written notice required | Day 45 |

| Foreclosure can legally begin | Day 120+ |

| OFA Resolution Conference | Before NOD is recorded |

| Notice of Default recorded | Often months after Day 120 |

| Notice of Trustee’s Sale served | At least 120 days before auction |

| Last day to reinstate loan | 5 days before auction |

| Trustee’s Sale (auction) | Approx. 150 to 200 days after NOD |

Total from first missed payment to auction: roughly 6 to 12 months, depending on lender’s pace.

How Portland Cash Buyers Helps You Sell Before the Auction

Selling your home before the auction can stop foreclosure entirely, protect your credit, and let you walk away with remaining equity. For homeowners working through the foreclosure timeline Oregon law establishes, the path you choose matters significantly.

A traditional listing takes 3 to 6 months, requires repairs and showings, and depends on buyer financing. For homeowners inside an Oregon foreclosure timeline, that process rarely fits the window remaining.

Portland Cash Buyers closes in 7 to 14 days. Owner Quinn Irvine has been buying homes directly from Portland-area homeowners since 2004 and handles every offer personally. There are no commissions, no required repairs, and no closing costs. Quinn buys with his own funds and does not wholesale or reassign contracts.

For homeowners facing foreclosure in Portland or already late on mortgage payments, a cash sale is often the only exit that protects both equity and credit.

The process is simple:

- Contact Portland Cash Buyers by calling (503) 770-0145 or filling out the online form. No paperwork or cleanup required.

- Receive a no-obligation cash offer within 24 hours. Quinn walks you through the math transparently.

- Close in 7 to 14 days. The title company settles your outstanding mortgage at closing. You keep the remainder.

Portland Cash Buyers is BBB A+ accredited and Google 5-star rated. Every closing goes through a licensed, insured title company.

Frequently Asked Questions About the Foreclosure Timeline Oregon

How long does the foreclosure timeline in Oregon take from start to finish?

From first missed payment to auction, the Oregon foreclosure timeline typically runs 6 to 12 months. The nonjudicial process alone takes about 150 to 200 days from the Notice of Default to the trustee’s sale.

Can I sell my home after I receive a Notice of Default in Oregon?

Yes. Within the foreclosure timeline Oregon sets, you can sell at any point before the auction date. A cash buyer can close in 7 to 14 days, which fits comfortably inside the 120-day window after the Notice of Trustee’s Sale.

What happens if I ignore foreclosure notices in Oregon?

Your home will be sold at a trustee’s sale. You lose remaining equity, must vacate within 10 days, and the foreclosure remains on your credit report for up to seven years.

Is there a redemption period after a foreclosure sale in Oregon?

Not in a nonjudicial foreclosure. Once the trustee’s sale occurs, there is no right to reclaim the property (ORS 86.797). A judicial foreclosure does allow 180 days to redeem, but most Oregon residential foreclosures are nonjudicial.

How many payments do I have to miss before foreclosure can start in Oregon?

Federal law requires servicers to wait until the loan is more than 120 days delinquent before officially beginning the foreclosure timeline Oregon homeowners face (12 C.F.R. § 1024.41). Many Oregon lenders wait considerably longer before recording the NOD.

Oregon Foreclosure Timeline: Act Before the Auction Date Arrives

The Oregon foreclosure timeline gives homeowners meaningful protections, but those protections only matter if you use them before the auction date locks in. The mediation window, the reinstatement right, and the ability to sell all carry hard deadlines attached to them.

From the first missed payment, fees compound, equity shrinks, and options close. If you are behind on payments, holding a Notice of Default, or staring at a Notice of Trustee’s Sale, do not wait. A cash sale before the auction is often the only path that leaves you with equity instead of an empty record.

Portland Cash Buyers closes in 7 to 14 days, pays all closing costs, and delivers no-obligation offers within 24 hours.

Call (503) 770-0145 or get your no-obligation offer within 24 hours.